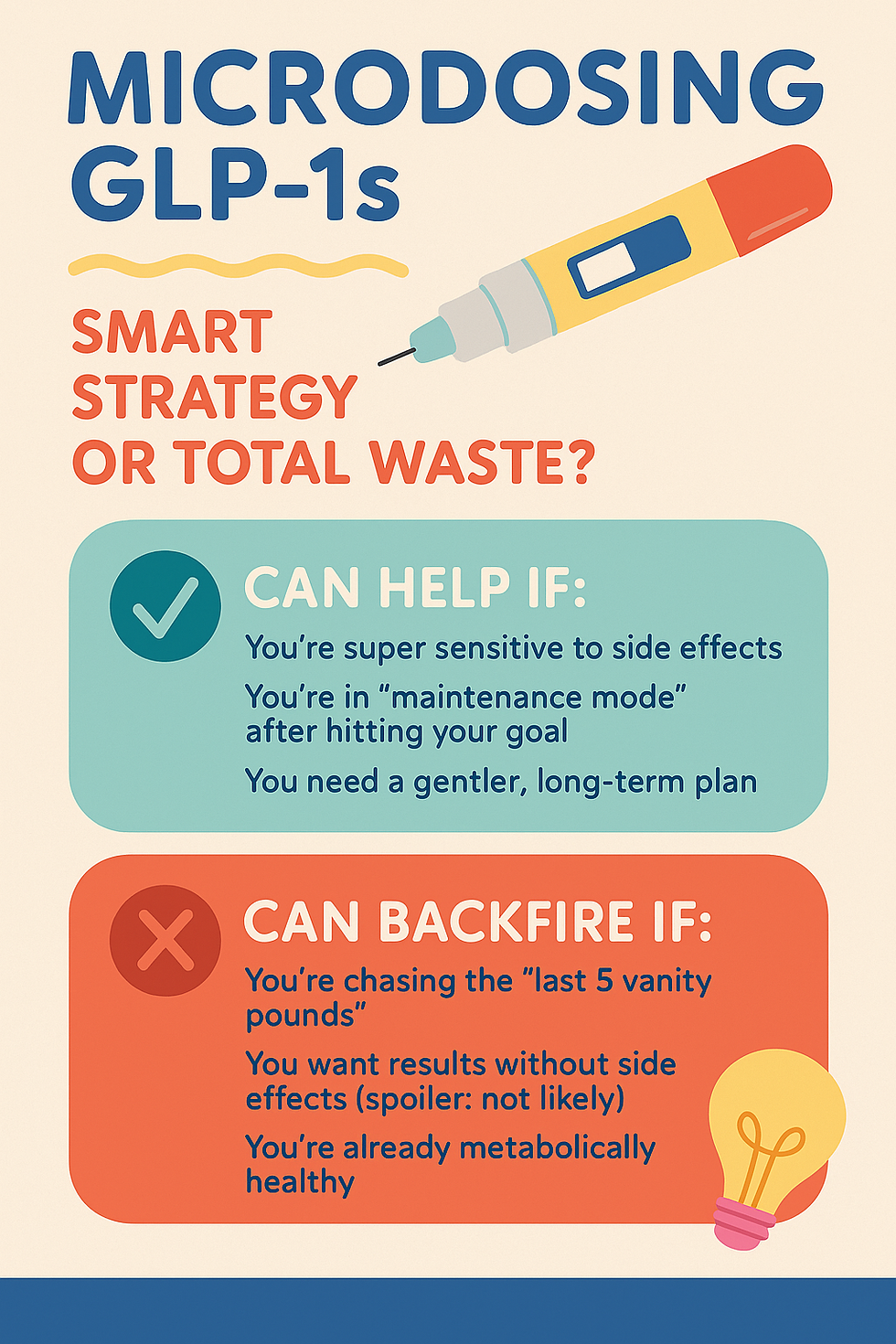

GLP-1s Could Save Your Life. Insurers Don’t Care.

- Julie Brownley, MD, PhD

- Aug 19, 2025

- 2 min read

GLP-1 medications (Ozempic, Wegovy, Mounjaro, Zepbound…) are revolutionizing obesity and metabolic health care. They reduce risk of diabetes, cardiovascular disease, and early death. But insurers? They slam the brakes on coverage. Why? Because the math looks bad for their bottom line.

Why Insurance Rarely Covers GLP-1s

Let’s cut through the PR. Insurers don’t deny GLP-1s because they don’t work — they deny them because they work too well and cost too much.

A major 2025 JAMA Health Forum cost-effectiveness study found that tirzepatide and semaglutide prevented tens of thousands of obesity, diabetes, and heart disease cases per 100,000 people. They added quality-adjusted life years (QALYs) — real, measurable health gains.

But here’s the kicker:

Tirzepatide’s cost-effectiveness ratio: ~$197,000 per QALY

Semaglutide’s ratio: ~$468,000 per QALY

In U.S. health policy, the accepted threshold for “cost-effective” is around $100,000 per QALY. Translation? Insurers argue that at current prices, these drugs aren’t “worth it.” The JAMA study showed tirzepatide would need a 30% price cut, and semaglutide an 82% cut, just to hit that mark.

From the insurer’s perspective:

Covering GLP-1s = huge short-term payouts.

Denying coverage = zero cost today, while future heart attacks, diabetes, or strokes fall on some other insurer down the line.

That’s why your denial letter feels like gaslighting.

Why the Process Feels So Opaque

The prior auth hoops? The vague denial letters? They’re not bureaucratic accidents — they’re intentional barriers. If patients or doctors give up halfway, insurers save millions.

What You Can Do to Fight Back

Get it in writing. Demand the exact coverage criteria.

Appeal like a lawyer. Use every denial as fuel for the next round.

Use your employer. HR departments can pressure insurers to expand obesity drug coverage.

Go public. Patient advocacy and social campaigns have moved the needle before.

How to Be Sure Your Doctor Is Fighting for You

A good doctor will:

Submit detailed prior auths with labs, BMI, comorbidity data.

Write strong letters of medical necessity.

Pursue appeals instead of dropping the fight.

If your doctor shrugs and says, “It’s not covered,” you’re not getting real advocacy.

Alternatives While You Wait

Manufacturer coupons: Some patients qualify for massive discounts.

Clinical trials: Free access if you qualify.

Avoid medspa markups: Many “wellness clinics” and online pill mills jack prices sky-high and push compounded drugs from questionable suppliers. Dangerous + overpriced.

Why Balance360 Is Different

At Balance360, we fight these battles with you:

Prior auth submissions and appeals? Done.

Coupon and patient assistance navigation? Covered.

Protection from predatory medspa pricing? Absolutely.

Because your health shouldn’t hinge on whether an insurance exec decides you’re worth it.

🔥 Bottom line: Insurers use cost-effectiveness math as a shield, but it’s really about protecting their wallets. At Balance360, we know the research, we know the fight, and we know how to get you access without the scams.

Comments